What Is Credit History and How to become creditworthy?

7 Tips to enhance your credit score and become creditworthy

A good credit score is a doorway to get a wide spectrum of loan & credit card approvals. But to open the line of credit, you need to build a credit history the right way.

It may appear challenging to maintain healthy creditworthiness, but it isn’t hard once you know where to begin. Higher credit ratings are a little more difficult to come by, but we’ll guide you on how to achieve the same.

Credit is a crucial part of one’s financial life, and building one’s credit history will be the first step if you’re new to the financial world and looking to avail credit for any personal or business need.

The problem is that many businesses want to verify your credit history before agreeing to give offer you a loan or credit card, and they may be wary if you don’t have one. There are a few options for getting over this possible stumbling block. Continue reading for some helpful advice on how to build credit from the ground up.

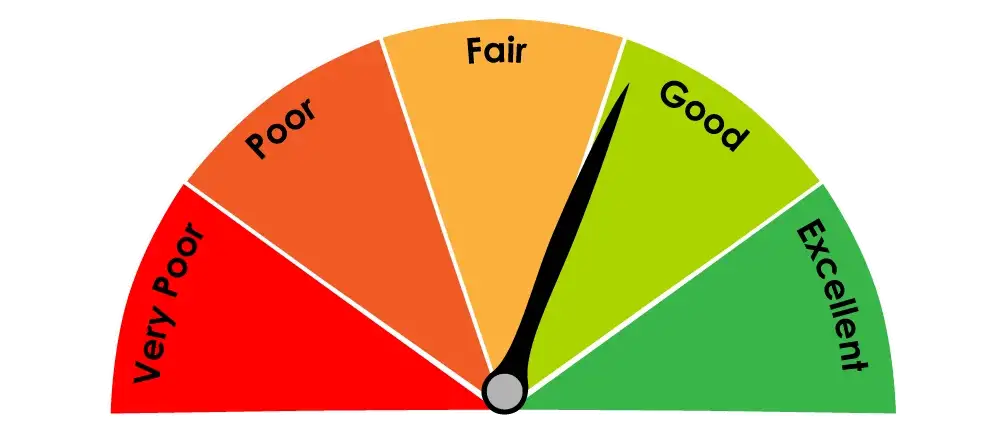

What Is A Credit History?

It is a record of your ability to repay debts and demonstrate responsibility in repaying them.

What all Information is Captured in Credit History?

A credit report includes information about the Number and types of your credit accounts Credit score Info like how long each account has been open, amounts owed, amount of available credit used, Details like whether credit card bills were paid on time, and the number of recent credit inquiries.

Users reap valuable rewards for having a good credit history, such as being offered lower interest rates on mortgage loans and car insurance.

Why building a credit profile is so important?

When you apply for a new financial product, such as a loan or a credit card, lenders will do a credit check. They may only accept candidates who meet particular credit criteria, such as a strong or exceptional credit score.

If you don’t have a good credit score, you can miss out on a low-interest mortgage, personal loan, or credit card, and end up paying more over the course of the loan. However, if you create a solid credit score, you will be able to save money on interest payments and invest the money in your future.

You’ll need a strong or exceptional credit score to take advantage of credit card benefits. The finest credit cards provide annual dining and travel credits, as well as high rewards rates, lounge access, and other benefits.

Good or exceptional credit ratings can help you qualify for the best loan offers, finest deals and help you remain creditworthy.

Here are some helpful tips to assist you to build a strong credit profile:

Tip #1 Apply for a Credit Card

If you do not have a credit history, most lenders and credit card companies will hesitate to lend money to you. So you can start with

Unsecured Credit Card:

An unsecured credit card is the most common type of credit card. It doesn’t require a security deposit for approval but beginners usually cannot avail of it due to no past credit history, applicants must have good credit history along with a decent salary or income to prove their creditworthiness. If you’re earning handsomely, you can try applying for an unsecured credit card or else move to the next type of credit card, which you can avail of without trouble. If you don’t have a decent income, you can start with a secured credit card

Secured Credit Card:

It is apt for the people who frequently face rejection whenever they apply for a credit card. The reason could be lack of income or income proof, poor or no credit history/score, or any other. A secured credit card is issued against some collateral. Just like a secured loan, you will have to produce some security for the card issuer to get the card.

Banks and credit card issuers preferably offer secured credit cards against a fixed deposit with them. Simply open an FD with the bank and they will issue a secured credit card almost instantly. The bank usually fixes a minimum FD amount that needs to be deposited to avail the credit card.

Tip #2

Become an Authorized User

If someone in your family or relation owns a credit card, you can request them to make you an authorized user, but beware to spend the amount wisely as any discrepancy in paying the due amount may impact the credit score of the person whose credit card you’re using.

Tip #3

Avoid Applying for Multiple Credit Cards at Once

While applying for a credit card do ensure that you are not applying with multiple credit card issuers simultaneously. It may leave a bad impression on them and weaken your chance to get a credit card. Choose the bank or providers to whom you can demonstrate your ability to maintain a good credit repayment history. Always keep the balance low and pay it fully on time

Tip #4

Use Credit Card Regularly:

If you want to build a healthy credit profile, make sure to use your credit card regularly. You can plan to spend it on shopping or grocery stores at least once a month and keep it active. As it takes time to build a healthy credit score, regular use of credit while ensuring their timely repayments will help you build a good credit history.

Tip #5

Monitor Balance-to-limit Ratio

Your credit card comes with a maximum credit limit to spend with. When you start using a credit card, credit bureaus consider the balance-to-limit ratio to determine your credit score. The balance-to-limit ratio, also known as the credit utilization ratio, is the proportion of the credit limit and the amount you have spent using a credit card. Monitoring this ratio is important as it shows how disciplined you are in managing the available credit available. If you don’t want to give an impression of a credit-hungry person, try to limit your credit utilization ratio within 30%–40% of your total credit limit.

Tip #6

Pay Your Credit Card EMI’s Fully & On Time

The credit bureaus have not revealed the weightage given to different credit parameters, however, the debt repayment history is considered the most influential parameter. Therefore, it is advisable to pay your due EMI’s in full, without any delay or miss. Ensuring full and timely help you maintain a healthy credit score quickly.

Tip #7

Go for an unsecured credit card after 12 months

It may take six months or a year or so to build a good credit score and generate a credit report. So if you are not holding any unsecured card, do go for it after you have built a repo with the credit bureau. An unsecured credit card offers a better credit limit and more perks to avail

Remember!

If you are new to credit, building a healthy credit repo takes some disciplined and committed effort, but once you have done so, you need to be even more cautious of not over-leveraging it. Maintaining an excellent credit profile is tough, but if you follow the tips given above and regularly maintain a good repayment history you may make the most out of your credit cards and loans you avail.